As an observer of the capital markets over the past few decades, I’ve noticed that “market professionals” and investment advisors are generally selling a story about the future. Whether a bold prediction on the future price of gold or a more subtle discourse on why it’s a good time to buy Tesla, Uber or Apple.

They are all spinning a story. CNBC fills its airtime with money managers prognosticating on the future. Usually two or more talking heads with opposite viewpoints.

They want to convince you that they—the storyteller—somehow have sharper insight into the future than everyone else. They want you to play the game.

If you are buying an investment, someone else must be selling.

The Investors—Just the Facts

Personally, I’m a numbers guy and prefer to trust data over stories. I prefer empirical research and a testable invest approach.

I want my investment portfolio to benefit from the long-term growth of productive enterprises around the world. I want investments diversified across asset classes. I want a portfolio with a level of volatility I’m comfortable sticking with through market gyrations.

Consider before investing:

- Most active money managers don’t beat the benchmark—so you will generally earn a higher return investing in index funds than in actively managed mutual funds

- A fund’s expense ratio is a statistically significant predictor of fund performance; the lower the cost, the higher the expected return—you can control investment expenses by using low-cost index funds

- Diversification is the only “free lunch”—by investing in a portfolio of diverse asset classes, it is possible to earn higher expected returns for a given level of volatility

The Players—Are They Just Lucky?

When evaluating stock pickers—and the mutual funds they run—one of the big challenges is distinguishing between luck and skill. A standard practice is to compare a fund’s annual performance to an appropriate market benchmark (e.g., the S&P 500 index).

So, if a fund manager strings together 5 consecutive years of beating their benchmark, have they demonstrated exceptional skill or was it just luck?

Assuming a normal distribution of returns within the relevant asset class, a random selection of stocks has a 50% chance of beating the benchmark each year. Hence, exceeding the benchmark 5-years in a row should happen just by chance about 3% of the time.

Unfortunately, with over 10,000 funds available, at any time hundreds of funds should have a 5-year winning streak purely by chance.

Past performance is not a good predictor of future returns.

The challenge is by the time you have enough historical data to believe a manager has exceptional skill, it is probably too late.

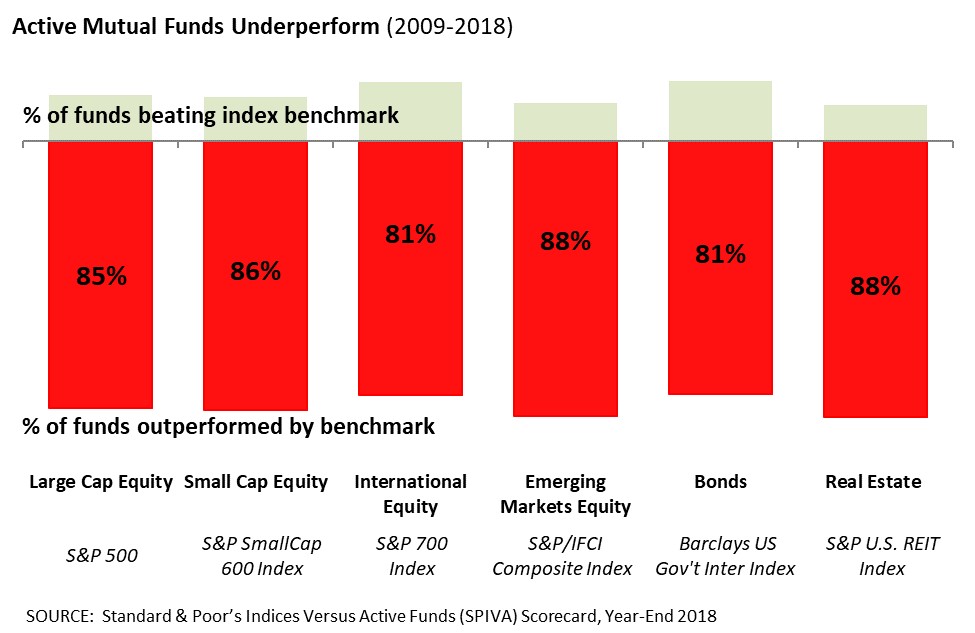

Active Management Underperforms

In a Standard & Poor’s study, over a 10-year period, over 80% of funds were unable to match or exceed their respective benchmark return after expenses (i.e., they under-performed).

Players Gonna Play, Play, Play

Some people appreciate getting calls from their broker with the latest “tip of the day.”

They enjoy hearing their broker spinning a story and like placing bets on the latest IPO, the direction of Pork Belly futures, or whatever the investment de jour is at their broker’s firm. C’est la vie.

These players enjoy being “in the game” and view buying and selling stocks as entertainment. And yes, it can be fun if you happen pick a big winner.

But is it investing?