Preferential Tax Treatment on Company Stock in Your 401(k)

If you hold shares of your employer’s stock in your 401(k) account, there is an IRS rule with the potential to significantly reduce your future tax burden. The rule pertains to net unrealized appreciation (NUA). NUA is the difference between the price you originally paid for a stock (i.e., your cost basis) and its current value.

This rule potentially applies to any employee who holds appreciated employer stock in their 401(k) account, but it’s particularly attractive for employees at technology companies with substantial appreciation in their firm’s stock price. For example, over the past 5 years (as of September 30, 2018), shares of many technology companies have experienced 200-500%+ gains:

- Amazon.com (+540%) — $313 to $2,003/share

- Microsoft (+240%) — $33 to $114/share

- Facebook (+230%) — $50 to $164/share

- Google (+170%) — $435 to $1,193/share

And this is just the past 5 years. If you are a longer tenured employee—especially at Amazon—and have been accumulating company stock in your 401(k), you could be sitting on even larger unrealized gains.

So What’s The Deal?

Normally, when you withdraw money from a tax deferred account (like a 401(k)), the money taken out is taxed as ordinary income at rates of up to 37% (unless it is rolled over to another qualified account). Although a 401(k) can defer taxes for decades, you eventually pay ordinary income tax rates on the investment gains and your pre-tax contributions. This taxation of all distributions as ordinary income[i] is the price you pay for the benefit of deferring taxes—and it’s generally a beneficial tradeoff.

But there is a potential loophole if you hold shares of your employer’s stock in your 401(k) account. If that stock has appreciated, you can qualify to only pay the lower long-term capital gains tax rate on the net unrealized appreciation (NUA) of the shares.

The distribution must be triggered by a qualifying event such as you leaving the company, reaching age 59 1/2, etc. After a triggering event, all the funds you hold in your 401(k) must be distributed in a single tax year (i.e., a lump-sum distribution).

To capture the benefit, one approach would be to transfer shares of your employer’s stock to a standard taxable investment account and rollover the remaining assets from your 401(k) to an IRA (to maintain the tax deferred status of these remaining assets).

Once you take the distribution of employer stock, you will owe Federal income tax at ordinary income rates (up to 37%), but only on the amount you initially paid for the shares of company stock (i.e., your cost basis). Which you would owe regardless when you eventually withdraw the funds. The tax benefit comes from only having to pay the preferential long-term capital gains rate (0%, 15% or 20%) on the remaining NUA (i.e., the value above your cost basis)—which you only pay once you sell the shares.

When you do decide to sell, the NUA amount is taxed at the lower long-term capital gains rate, regardless of how long you actually owned the stock. Any additional gains after distribution will be taxed under normal capital gains tax rules (i.e., short or long-term gain depending on the holding period).

A Hypothetical Example

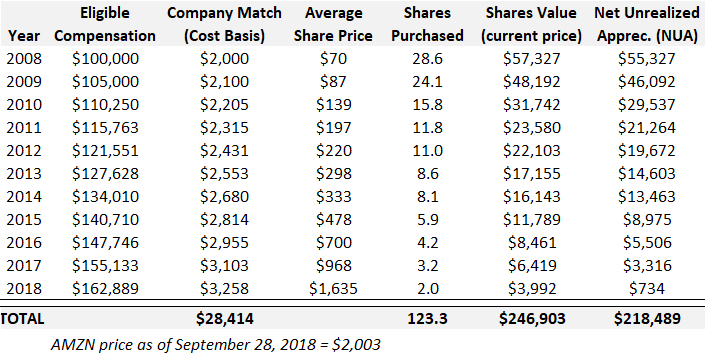

Jeff has been at Amazon for 10 years and elected to contribute 4% of his salary to his 401(k) plan. He opted to invest the 50% match (i.e., 2% of compensation) in the Amazon Company Stock Fund (which is only available as an investment option for company matching contributions). Assuming Jeff’s salary was $100,000 in 2008 and increased on average by 5% per year, he would have bought approximately 123 shares of company stock for $28,400 over the 10 year period. But the value of the company stock could now be worth nearly $250,000.

Now assume Jeff just turned 60 years old and decides to retire. He has the option to take a lump-sum distribution of the entire 401(k) account. The value of his 401(k) not invested in Amazon stock is distributed to a Rollover IRA and the shares of Amazon are directly transferred “in-kind” into a taxable investment account.

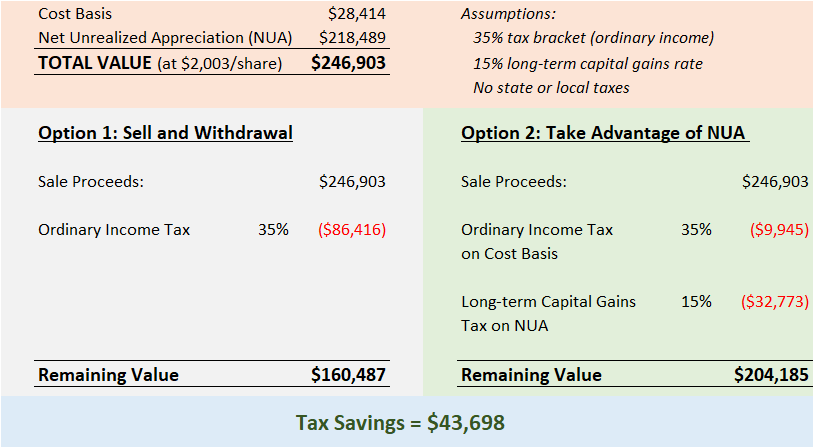

Following the distribution, Jeff owes tax on his cost basis for the Amazon shares—the $28,400 the shares cost when purchased inside his 401(k). Depending on his tax bracket, he likely owes income tax of between $6,820 (24%) and $9,940 (35%). But he now has the entire ~$250,000 of company stock in a taxable account—with only long-term capital gains due on the appreciation when he chooses to sell.

If Jeff wants to spend the money or invest in a more diversified portfolio, he can sell the Amazon shares. He will likely pay the 15% long-term capital gains rate (depending on his total household taxable income). Netting a tax savings of between 9% and 20% (approx. $20K to $44K)—assuming his tax bracket is between 24% and 35%—compared to selling and taking a cash withdrawal from his 401(k) account or Rollover IRA.

Simplistic Example: Two Options to Generate Cash from Company Stock Holdings

Additional benefit from on-going tax deferral can continue to accrue if Jeff waits and does not sell the shares immediately. He can continue holding the stock—letting it (hopefully) appreciate—while deferring payment of the capital gains tax until he sells. Even potentially selling shares slowly over his retirement years to keep his annual income in a low tax bracket.

“The ability to potentially pay the lower long-term capital gains tax on NUA can help you significantly save on taxes when you need to withdraw money from your retirement account.”

Specific Requirements

- Must be a lump-sum distribution from your 401(k)—all funds in the account need to be removed/transferred during a single tax year.

- Distribution must be “in-kind” of actual shares of your employer’s stock (not phantom stock or another proxy). Company Stock Funds also generally qualify as long as they only hold company stock and cash, and the plan will distribute actual shares. Shares should be transferred directly to a standard taxable brokerage account. You must actually receive shares of the company stock even if you plan to immediately sell them.

- Must be done after a triggering event (separation of service, reaching age 59 ½, etc.)

Who is Most Likely to Benefit?

- Those with significant net unrealized appreciation (NUA) in company stock—the higher the percentage gain, the greater the benefit, since a larger percentage of the distribution will be taxed at the preferential long-term capital gains rate.

- Those over age 59 ½ to avoid the 10% early withdrawal penalty.

- Those who have a near term need for the money—if you don’t need the funds for a substantial time, the benefit from continued tax deferred growth in an IRA may outweigh the tax savings.

- Those living in states with low or no state income tax since state income tax is often applied equally to ordinary income and capital gains, dampening the potential benefit.

- If you believe your future tax rate will be equal to or greater than the rates you pay today (if you believe your future tax rate will be significantly lower than your rate today, it may be better to maintain the funds in your tax deferred 401(k) and forego the NUA benefit).

- Employees at companies that offer company stock as a standard investment option in your 401(k).

Potential Drawbacks to Remember

- Must immediately pay income tax on your cost basis at ordinary income tax rates

- If you sell shares after distribution—for example, if you need the money or want to diversify your investments—you will immediately be hit with a capital gains tax bill

- You lose tax deferred status on the investments transferred out of a qualified account

- If you have not reached 59 ½ years old, you may be assessed a 10% early withdrawal penalty

The benefits from the NUA provision can be significant depending on your situation, but it’s not always straightforward. The various rules, options, and alternatives create a complicated decision. Rules are complex and unforgiving, and the impact of this decision can spill over into other aspects of your financial plan, like your overall investment strategy and estate plan. You should consult your tax advisor to determine applicability to your specific situation.

For more details on how to claim this tax benefit, please review IRS publication 575, Pension and Annuity Income.

(i) As opposed to investment returns being taxed at lower rates as either long-term capital gains or qualified dividends.