Today, we’re focusing on a pivotal age: wealth at age 55.

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

At this stage of life, you’ve likely been building your financial foundation for decades. It’s important to gauge your progress, compare your wealth, and evaluate your investments to ensure a secure retirement.

Let’s dive into what you should have accumulated by age 55, keeping in mind that each person’s journey is unique.

When saving for retirement, the question is often “how much should I have saved at my age?”

Ideally, this question would be answered in the context of a comprehensive financial plan. A plan that accounts for the lifestyle desired in retirement, target retirement age, current wealth, and other personal factors.

But who has time for all that detail!?

Experts would say that at 55 years old, you should have saved 6 to 7x your income for retirement.

What? Why? Where did that number come from?

This article digs into this question in more depth. We provide various viewpoints how much savings the typical 55-year-old should have to be on target for a comfortable retirement. All without getting too bogged down in details.

We also explore why the conventional wisdom / expert guidance on retirement accumulation doesn’t make sense at younger ages. And, why the power of compounding investment returns is your best friend when saving for retirement.

The “Experts” POV

CNBC.com addressed this vary issue in “Here’s how much cash you should have saved at every age.”

According to this article—which references guidelines from Fidelity Investments—you need to have savings equal to 10 times your income if you want to retire at age 67 (when individuals under 60 today will be eligible for full social security benefits). Save more if you want to retire earlier and less if you can keep working until you are 70.

They breakdown the savings target by age to reach 10 times your income:

- Age 30 = 1x income

- Age 40 = 3x income

- Age 50 = 6x income

- Age 60 = 8x income

- Age 67 = 10x income

Hence, at 55-years-old you should have savings of around 7x your income (the halfway point between savings at age 50 and 60) according to Fidelity Investments.

Millionaire Next Door

In Thomas Stanley and William Danko’s book, The Millionaire Next Door, they provide a simple formula to determine if you are an “average accumulator of wealth” (AAW). Basically, their name for people who are doing a good job building wealth.

Their formula for an AAW is:

“expected” net worth = (income X age) / 10

For example, if you are 55 years old and your household income is $100,000, you should have saved $550,000 (= $100,000 x 55 / 10). Or 5.5 times your income.

Interestingly, for a 55-year-old, Fidelity and The Millionaire Next Door have fairly different suggestions for how much you should at this point in life. In general, the AAW target is higher than other “experts” when you are young, but a lower total target when you are older.

But it Makes No Sense

The problem is neither of these–fairly linear–approaches align with how wealth grows. If someone saves a constant percent of their income for retirement (e.g., through contributions to a 401k plan) and their income grows steadily throughout their career, the growth trajectory is not linear.

Due to the benefits of compound interest (or compounding investment returns), as you accumulate more wealth for investment, a higher percentage of your annual increase in wealth will come from investments returns as opposed to new savings.

Fidelity’s guidelines propose you should triple retirement savings (as a multiple of your income) during your 30s and double it during your 40s. But Fidelity only targets growing retirement savings by 33% during your 50s (from 6x income to 8x…a 33% increase) and 25% during your 60s. How does this make sense?

If you managed to accumulate 6x your income by the time you reach age 50, investment returns alone over the next decade—under normal circumstances— should easily grow your savings by over 33% during the next 10 years. Even if you assume only a 5% annual return (which is well below historical norms for a diversified portfolio), your portfolio should grow by 63% in 10 years (pre-tax).

Income Also Increases

Since the retirement savings targets are provided as a multiple of current income, you also need to account for your income increasing over time. So, the comparison is not as simple as shown above.

If your income increases at 3% per year, your annual income would be 34% higher after a decade. If your household income is $100,000, after 10 years you would have income of $134,000/year.

Following Fidelity’s guidelines, you should target $600,000 in retirement savings (6x your $100,000 household income) at age 50. And at age 60 you should target $1,070,000 (8x your $134,000 in household income after 10 years).

Hence the actual increase in savings over the decade needs to be 78% and not the 33% previously reference.

But still, growing your savings by 78% over a decade is far easier when your investment portfolio is providing most of the increase.

Contrast this with trying to (3x) triple your retirement savings during your 30s when you have very little savings to begin with. In this scenario, most of the increase in savings needs to come from socking away more money from earnings.

The Wealth45 Approach

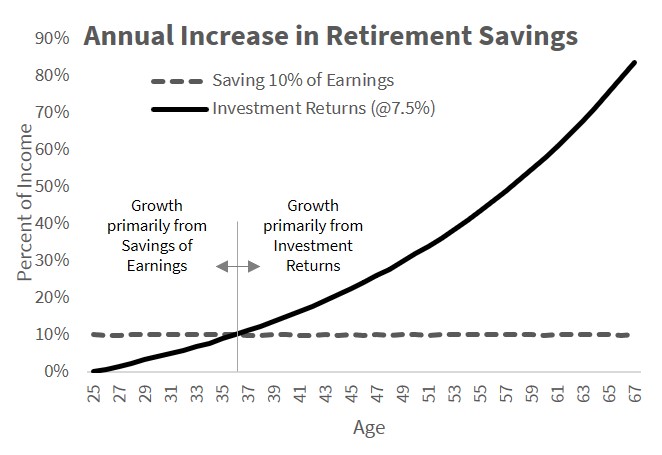

A more realistic approach is to recognize the compounding effects of investment returns and build a plan based on saving a fixed percentage of your earnings every year. We believe this provides a more rational approach to retirement savings.

If you constantly saving 10% of your income and invest it, the annual increase in retirement savings becomes dominated by investment returns as you get closer to retirement—making it easier to grow your retirement savings faster once you have an established nest egg.

(graph based on assumptions outlined below for the Wealth45 guidelines)

(graph based on assumptions outlined below for the Wealth45 guidelines)

Furthermore, we believe you should target more like 12x your income at retirement (see Roadmap to Retirement: FIRE or FRA for details).

Although 10x is a reasonable goal, your target should provide a cushion to account for unforeseen circumstance. The primary hazard being many people retire earlier than planned due to health issues, layoffs, or other uncontrollable events.

The Wealth45 breakdown of savings by age to reach 12 times your income:

- Age 30 = <1x income

- Age 35 = 1 to 2x income

- Age 40 = 2 to 3x income

- Age 45 = 3 to 4x income

- Age 50 = 4 to 5x income

- Age 55 = 6 to 7x income

- Age 60 = 8 to 9x income

- Age 65 = 10 to 11x income

- Age 67 = >12x income

Our guidelines are based on the following assumptions:

- Start saving for retirement at age 25

- Target retirement at age 67 (Full Retirement Age of those born after 1959)

- Household income grows at a steady rate throughout career (e.g., 3% annually)

- Constant savings rate (as % of income) throughout career (e.g., 10% including 401k match)

- Investment returns of 7.5% annually

Wealth45 vs “Expert” Guidance

Although our savings targets by age are not wildly different from the “experts,” there are a few important differences.

At age 55, we believe an appropriate target is between Fidelity and The Millionaire Next Door (TMND).

| Multiple of Income | Wealth45 | Fidelity | TMND (AAW) |

| Age 55 | 6.5x | 7x | 5.5x |

In general, the Wealth45 savings targets are lower when you are young and have just started to save for retirement. But our targets accelerate faster when you are older and have built-up a comfortable nest eggs (and returns on your investments becomes the primary growth engine).

The crossover point is somewhere in your mid to late 50s where Fidelity and Wealth45 agree on the target. Before this age, Fidelity is recommending a higher savings as a multiple of income. Afterward, Wealth45 believes you should target a slightly higher multiple of income.

Reality Disconnect

Unfortunately, for most people these savings targets are completely unrealistic and disconnected from their reality. The majority of people in the United States have nowhere near this level of savings.

Data from the latest Federal Reserve Survey of Consumer Finances (2019):

| Age of head | Median Net Worth (‘000) | Median Income (‘000) |

| 35-44 | $91 | $73 |

| 45-54 | $169 | $78 |

| 55-64 | $213 | $66 |

Using the data above to calculate the net worth as a multiple of income:

| Age of head | Multiple of Income |

| 35-44 | 1.2x |

| 45-54 | 2.2x |

| 55-64 | 3.2x |

Clearly these savings multiples for median households are far below the targets proposed. And even these figures are too optimistic since median net worth is not the same as retirement savings.

For many people, the largest asset is their primary residence (i.e., the equity in their home). Although some people can downsize at retirement and live off the proceeds, this is easier said than done.

Luckily, as a group, employees of technology firms are outliers to the general population, earning high salaries and able to save more toward retirement.

Stay tuned for a future post on what to do if you are 55 and not on-target to hit your retirement goals. Sign-up here for our emails.

How to Set Yourself Up for Success

If you are fortunate enough to be able to save for retirement, there is a formula for long-term success.

- Start young – the earlier you can start socking away money for investing, the easier it is to reach your retirement goals

- Save a fixed percentage of your income every year – target 10%

- Invest your savings in a diversified portfolio aligned with your risk tolerance and time horizon (click here to find your portfolio)

A simple way to implement this formula is to take advantage of your employer’s 401k plan (if you work for a company like Microsoft, Amazon, Google and most other large employers that provide matching contributions).

The company match will reduce the amount of money you need to save and help grow your retirement savings faster.

- Microsoft chips in (i.e., matches) 50 cent for every dollar you contribute (up to the max IRS limits). Hence, if you contribute 7% of your income, Microsoft will provide an additional 3.5%, putting your total savings at 10.5% annually.

- Amazon.com matches 50% on the first 4% of your contributions (for a total of 2%). Hence, you will need to contribute 8% of your salary to reach the 10% goal once Amazon chips in their 2%.

- Google will also match 50% on the dollar, with the added advantage of a 100% match on the first $3,000 in contributions. Hence, depending on your salary, you will need to contribute between 5% and 7% to reach the desired 10% overall savings rate.