A comfortable retirement—with ample assets—is the ultimate savings goal. Sacrifice consumption today so that one day you are financially independent and can retire with a fulsome lifestyle.

Early retirement advocates have adopted the acronym FIRE (Financial Independence, Retire Early) as their rallying cry.

The FIRE movement largely focuses on limiting expenses—living on a fraction of your income—to maximize money socked away for investment. With the added benefit that living on a lower burn rate reduces the amount of money needed to support your lifestyle once you stop working.

The roots of the FIRE movement can be traced back to the book Your Money of Your Life by Joe Dominguez and Vicki Robin. It was first published in 1992 but has recently had renewed popularity.

More traditionally, FRA refers to Full Retirement Age. This is the age you are eligible for full Social Security benefits (reduced benefits may be available at age 62).

Retiring near your FRA greatly reduces the amount of savings required to maintain your lifestyle. Instead of relying solely on your investment income to cover expenses—by waiting until your mid-60s to retire—you gain both income from Social Security and reduced expenses from Medicare benefits.

Financial Independence

If financial independence is your primary investment goals, a few questions naturally arise:

- How much do I need to be saving each year?

- How much should I have saved at this point in my life?

- When will I be financially independent?

The answers to these questions depend on many factors and no magic formula can definitively declare if you are on-track.

The age you want to retire, your burn rate (i.e., annual expenses), and income expected from other sources (such as a pension or Social Security) will largely determine how much you need to save.

Savings Guidelines

Based on assumptions detailed below, I took a crack at developing targets to help guide your journey to financial independence at retirement. These are strictly guidelines; everyone’s situation is different and should be individually evaluated.

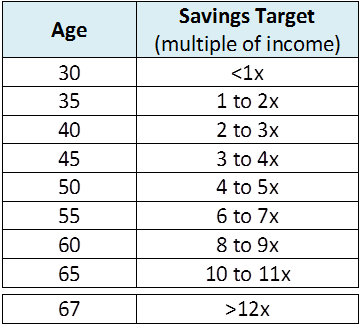

The table below shows rough targets, by age, of the investable assets you should aim to accumulate if you plan to retire at age 67 (i.e., full retirement age for those born after 1959).

Asset targets are listed as a multiple of current income. For example, if your household income is $50,000 and you are 40 years old, your savings target should be $100,000 to $150,000.

These targets assume you start saving for retirement at a relatively young age and your savings, as a percentage-of-income, remains constant throughout your career (e.g., you save 10% of income each year).

Some people may find this assumption unrealistic given the higher financial demands, relative to income, on younger people who may be paying off student loans, raising a family, and buying their first home.

Build Your Savings Muscle

Although it might appear easier to wait and start saving later in your career when income is higher, the earlier you start saving—and not spending all your income, or worse, taking on consumer debt—the easier you will find it in the long run. Plus, you never know what the future might hold.

Save what you can. Build a nest egg. Increase your financial security.

We recommend saving at least 10% of your income toward retirement each year—including any 401(k) contribution your employer provides—assuming you start saving in your 20s.

For example, if your employer provides a 50% match on your 401(k) contributions, you would set your contribution at 7%. Your 7% contribution, plus your employer’s 3 ½% matching contribution would put you over the 10% retirement savings target.

If you work for a company—like Amazon.com—that limits matching contributions to the first 4% of annual compensation, you would need to contribute 8% to your 401(k). Your 8% contribution, together with Amazon’s 50% match on the first 4% (i.e., an additional 2% of compensation), would equal the 10% retirement savings target.

If you wait to start saving for retirement until later in your career, you will need to target a higher percentage of income.

Replacing Income

Our calculation assumes a retiree needs income equal to 75% of their final working salary to maintain the same lifestyle. Once retired, you are no longer saving 10%+ of your income toward retirement, no longer paying payroll taxes, and potentially in a lower income tax bracket.

We also assume Social Security benefits will replace about 25% of your pre-retirement income (an optimistic assumption for those with higher income).

Hence, you need to replace 50% of your pre-retirement income with investment income.

Using the “4% rule” for spending in retirement, implies you need assets equal to about 12.5 times your income when you retire.

If your goal is to retire young—and live the FIRE principals—you should target 25x your annual burn rate as a savings target.

The Millionaire Next Door

For comparison, we have added the suggested wealth accumulation targets from Thomas Stanley and William Danko’s book, The Millionaire Next Door.

The authors suggest a simple formula to determine if you are an “average accumulator of wealth” (AAW):

“expected” net worth = multiply your income by your age and divided by 10.

For example, if you are 40 years old and your household income is $75,000, you should have saved $300,000 (= $75,000 x 40 / 10).

“Builders of Wealth”

The book also defines “prodigious accumulators of wealth” (PAW) as people who double these thresholds (i.e., saved $600,000 in the example above).

Although this simple formula seems reasonable for people mid-career, it is a little unrealistic for younger folks and the AAW numbers are potentially too conservative (low) for people approaching retirement.

| Age | Wealth45 (multiple of income) | Millionaire Next Door (AAW to PAW) |

| 30 | <1x | 3 to 6x |

| 35 | 1 to 2x | |

| 40 | 2 to 3x | 4 to 8x |

| 45 | 3 to 4x | |

| 50 | 4 to 5x | 5 to 10x |

| 55 | 6 to 7x | |

| 60 | 8 to 9x | 6 to 12x |

| 65 | 10 to 11x |

When Do You Plan to Retire?

Most people probably think of standard retirement age as 65. For many years this was when full Social Security and Medicare benefits kicked in.

For people retiring today, full retirement age for Social Security is 66, rising to 67 for younger generations (and likely to be raised even higher as life expectancy increases and Congress seeks ways to reduce expenditures).

Yet studies have concluded that up to half of all workers end up retiring before they planned. Over a third of all beneficiaries start claiming Social Security benefits at 62.

Layoffs, health problems, or a multitude of other unforeseen complications can lead to an unexpected early retirement.

Frontload your retirement savings as much as possible and don’t plan to “catch-up” in your late 50’s and early 60’s.

1 Comments

[…] we believe you should target more like 12x your income at retirement (see Roadmap to Retirement: FIRE or FRA for details). Although 10x is a reasonable goal, your target should provide a cushion to account […]

Reply