With the Federal Reserve “printing” massive amounts of new money to fund Congress’s record-breaking deficit spending, I thought it would be a good time to review investments considered good hedges for inflation. Ideally a good inflation hedge would maintain (or increase) its real value during periods of high inflation.

Today’s post will consider Treasury Inflation-Protected Securities (TIPS). These are debt securities issued by the United States with a payout determined by the level of future inflation. The idea being holders of this debt will get a fixed real return (i.e., a fixed return above inflation) regardless of future inflation.

Future posts in the Wealth45 Inflation Hedge Series will consider other common inflation hedges such as gold, real estate, value stocks, etc.

Current Situation

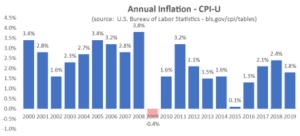

Although inflation has been low over the past decade, there are reasons to believe future inflation could be much higher.

The Federal Reserve has been actively working to increase inflation to meet their 2% annual inflation target. Recently the Fed changed policy and stated they are willing to let inflation run above the 2% target before they will move to increase interest rates. Setting the stage for higher inflation without a policy response.

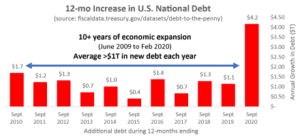

Additionally, the U.S. government has continued its deficit spending spree and exploded the national debt to around $27 trillion (about 1.2x pre-recession GDP).

Even before this year’s massive spending in response to the COVID pandemic, Congress ran $1+ trillion annual deficits (and this is 10 years into an economic expansion!)—throwing out the window any sense of fiscal responsibility or fallacy of following a Keynesian economic policy (i.e., deficit spending to stimulate the economy during a recession).

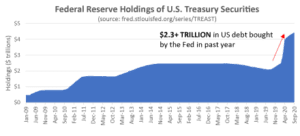

And finally, the Federal Reserve has gone on an unprecedented binge of buying the debt created by this deficit spending spree (see chart below). In effect the Fed is monetizing the national debt by “printing” more money. This should—at least theoretically—create an inflationary environment.

Considering these factors—together with the rise in financial asset prices (stocks, bonds, etc.) that we have already seen—it is understandable that investors are looking for an inflation hedge. Although no one knows what the future will bring, a bout of higher inflation is certainly a reasonable bet.

How do TIPS Work

To quote the Treasury website:

“TIPS provide investors with protection against inflation. The principal of a TIPS increases with inflation and decreases with deflation, as measured by the Bureau of Labor Statistics Consumer Price Index for All Urban Consumers (CPI-U)”

“When a TIPS matures, the investor is paid the inflation-adjusted principal or original principal, whichever is greater. Since a TIPS investor won’t receive less than the original principal, the investor’s original principal amount is protected against deflation as well.

TIPS pay interest semiannually at a fixed rate. The rate is applied to the adjusted principal; so, like the principal, interest payments rise with inflation and fall with deflation.”[i]

Are TIPS a Good Inflation Hedge?

As mentioned above, TIPS are a debt instrument that normally pays the holder both a fixed interest payment every 6 months (semiannually) and a principal adjustment based on the level of inflation experienced. The desired outcome being the debt holder receives a stable, real (inflation-adjusted) return.

The holder is protected from inflation risk, which for long-term, fixed income debt, can be a major risk.

On the surface, it would seem like TIPS would be the perfect inflation hedge. Your return is completely protected from inflation and you know your inflation-adjusted income over the term of the security.

The Problem with TIPS

The problem is TIPS currently trade at a negative yield. Instead of providing a fixed return above future inflation, they now lock in a negative real (inflation-adjusted) return.

For example, the latest auction of 30-year TIPS in August 2020 resulted in a median coupon yield of (0.38%). Locking in an inflation-adjusted loss for bond holders of 3/8 of a percent each year for the next 30 years.[ii]

Even more dramatic, bond holders locked in almost a 1% annual inflation-adjusted loss on the 5-year TIPS auctioned in July 2020. [iii] With these 5-year TIPS, you need an inflation adjustment of nearly 1% annually to just maintain your principal and break-even.

Conclusion

With TIPS, if inflation unexpectedly spikes, your investment will likely do better than conventional fixed coupon debt and potentially lose less money than some other investments. But you will lose money on an inflation-adjusted (real) basis—it is guaranteed by the negative yield.

On the positive side, it may be better to lose a little money than risk losing a lot of money. Basically, with TIPS today, you are locking in a small, inflation-adjusted loss for protection against a larger loss that might be seen in other fixed income investments (or by holding cash) when inflation spikes.

[i] https://www.treasurydirect.gov/instit/marketables/tips/tips.htm

[ii] https://www.treasurydirect.gov/instit/annceresult/press/preanre/2020/R_20200820_3.pdf

[iii] https://www.treasurydirect.gov/instit/annceresult/press/preanre/2020/R_20200710_1.pdf

2 Comments

[…] discussed in my prior post, Are TIPS a Good Investment, TIPS are designed as an inflation hedge. Your return is fully protected from inflation since the […]

Reply[…] discussed in my prior post, Are TIPS a Good Investment, TIPS are nearly the perfect inflation hedge. Your return is fully protected from inflation since […]

Reply