International stocks have been crushed by U.S. stocks over the past decade—and the return from developed international markets has barely outpacing inflation over the past 20 years.

Leading some investors to question if they should own foreign equities given this poor performance. For a variety of reasons, we still believe U.S. investors should maintain exposure to international equities.

We claim no ability to “call” a bottom or an impending bounce in these investments. A reversal could happen quickly or take years to play out. But we do believe underperforming markets will eventually make-up lost ground and provide a more typical long-term return.

Why International Investing?

The U.S. Securities and Exchange Commission (SEC), highlights two of the chief reasons why U.S. based investors hold investments with international exposure:

- Diversification—spread investment risk across both foreign and U.S. companies

- Growth—take advantage of the potential for growth in foreign economies, particularly emerging markets

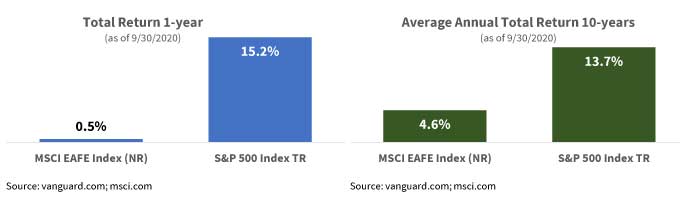

International Equity Growth

Admittedly, international investments have not performed well recently. The MSCI EAFE Index—an equity index representing 21 developed markets around the world, excluding the U.S. and Canada—has trailed the S&P 500 Index by over 9 percentage points per year for the past decade.

The good news is the valuation of international stocks is low relative to large, U.S. companies.

According to MSCI, the price-to-earnings (P/E) ratio of the EAFE index is 20 (forward P/E <17) and the dividend yield is relatively high at 2.7%. Compare this to the S&P 500 index with a P/E of over 31 (forward P/E of 22) and a dividend yield of just 1.7% (as of 9/30/2020).

One never knows what the future will bring, but the valuation of international stocks is low relative to domestic stocks—potentially portending high future growth.

Returns Move Around

Even as large U.S. stocks dominated global returns over the past decade, there have been years where international stocks did better. In three of the past 10 years, emerging markets outperformed large-cap U.S. equities. And in two of these periods, even developed international stocks bested domestic.

Regardless of the challenges faced, we believe maintaining a well-diversified portfolio with exposure to broad asset classes is the best approach. It is not news that some euro zone countries are having challenges and China’s growth is slowing.

If anything, the market often overreacts and there is potentially more upside opportunity than additional downside risk.

Just as a great company is not necessarily a great stock to own, the current economic situation does not necessarily imply international stocks are a bad investment at today’s prices.

Investment Principals

Let us highlight three important investing principals:

1) maintain a globally diversified portfolio

2) rebalance regularly to keep the appropriate risk exposure and potentially gain from market volatility

3) be mindful of regression to the mean

Stay Diversified

Long-term investors should maintain a diversified portfolio of global equities (both domestic and international), bonds, and alternative assets. Your asset class mix should reflect your willingness and ability to accept the inevitable ups and downs of the market.

The more volatility an investor is willing to endure, the higher their allocation can be to equities and other securities with higher expected returns (and the commensurate increased level of risk).

Different investments perform well at different times. By maintaining a diversified portfolio, one can capture overall market returns over time while smoothing out the downturns. When one investment category is performing poorly, hopefully your other investments are doing better.

Technically, this involves investing in a collection of low-correlation asset classes. A diversified portfolio of low-correlation assets has historically provided a higher return for the same level of risk compared to investing in less diversified investments.

Rebalance to Benefit from Volatility

A regular rebalancing cycle has two benefits: 1) maintains the appropriate portfolio risk level, and 2) improves long-term returns by systematically trimming overvalued assets and buying temporarily undervalued assets.

Rebalancing effectively allows investors to “sell high” and “buy low.”

Rebalancing a portfolio involves selling assets which exceed their target allocation percentage and buying assets which are below their target.

For example, if Treasury bonds have increased substantially in value and international stocks have plateaued (as seen over the past 20 years or so), your portfolio may have a materially higher percentage of assets invested in Treasury bonds than desired and a lower percentage in international stocks. Rebalancing sells part of the bond holdings and buys more international stock, returning the portfolio to its target composition.

Regression to the Mean

In investing terms, “regression to the mean” refers to the tendency of asset classes to generate returns above their historical average following a period of below-average performance (and vice versa).

When an asset class has an exceptionally poor run—such as developed international stocks over the past 20 years—it is often the case that future performance will be superior. Resulting in a combined return more in-line with long-run historical performance.

Of course, this also applies to asset classes which have recently performed well (e.g., large U.S. technology stocks); there is a good chance that future performance will be inferior, bringing overall returns closer to the long-term average.

Share Your Thoughts